UNIVERSAL KNOWLEDGE HUB

SOURCE - CLICK HERE TO VIEW

[TO BE PUBLISHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II,

SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

[CENTRAL BOARD OF DIRECT TAXES]

Notification

New Delhi, the 23rd day of September, 2013

INCOME-TAX

S.O. 2887(E).- In exercise of the powers conferred by sections 101 and144BA read with

section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby

makes the following rules further to amend the Income-tax Rules, 1962, namely:-

1. (1) These rules may be called the Income-tax (17th Amendment) Rules, 2013.

(2) They shall come into force on the 1st day of April, 2016.

2. In the Income-tax Rules, 1962, –

(a) after rule 10T, the following rules shall be inserted, namely: -

“ DA. Application of General Anti Avoidance Rule

Chapter X-A not to apply in certain cases

10U. (1) The provisions of Chapter X-A shall not apply to -

(a) an arrangement where the tax benefit in the relevant assessment

year arising, in aggregate, to all the parties to the arrangement does

not exceed a sum of rupees three crore;

(b) a Foreign Institutional Investor, –

(i) who is an assessee under the Act;

(ii) who has not taken benefit of an agreement referred to in

section 90 or section 90A as the case may be; and

(iii) who has invested in listed securities, or unlisted securities,

with the prior permission of the competent authority, in

accordance with the Securities and Exchange Board of India

(Foreign Institutional Investor) Regulations, 1995 and such

other regulations as may be applicable, in relation to such

investments;

(c) a person, being a non-resident, in relation to investment made by

him by way of offshore derivative instruments or otherwise,

directly or indirectly , in a Foreign Institutional Investor;

(d) any income accruing or arising to, or deemed to accrue or arise to,

or received or deemed to be received by, any person from transfer

of investments made before the 30th day of August, 2010 by such

person.

(2) Without prejudice to the provisions of clause (d) of sub-rule (1), the provisions of

Chapter X-A shall apply to any arrangement, irrespective of the date on which it

has been entered into, in respect of the tax benefit obtained from the arrangement

on or after the 1st. day of April, 2015.

(3) For the purposes of this rule, -

(i) “Foreign Institutional Investor” shall have the same meaning as assigned to

it in the Explanation to section 115AD;

(ii) “off shore derivative instrument” shall have the same meaning as assigned to it in the Securities and Exchange Board of India ( Foreign Institutional Investor) Regulations, 1995 issued under Securities and Exchange Board of India Act, 1992 (15 of 1992) ;

(iii) “Securities and Exchange Board of India” shall have the same meaning as assigned to it in clause (a) of sub-section (1) of section 2 of the Securities and Exchange Board of India Act, 1992 (15 of 1992);

(iv) “tax benefit” as defined in clause (10) of section 102 and computed in

accordance with Chapter X-A shall be with reference to-

(a) sub-clauses (a) to (e) of the said clause , the amount of tax; and

(b) sub-clause (f) of the said clause, the tax that would have been

chargeable had the increase in loss referred to therein been the total

income.

Determination of consequences of impermissible avoidance arrangement.

10UA . For the purposes of sub-section (1) of section 98, where a part of an arrangement

is declared to be an impermissible avoidance arrangement, the consequences in relation

to tax shall be determined with reference to such part only.

Notice, Forms for reference under section 144BA

10UB. (1)For the purposes of sub-section (1) of section 144BA, the Assessing

Officer shall, before making a reference to the Commissioner, issue a notice in writing to

the assessee seeking objections, if any, to the applicability of provisions of Chapter X-A

in his case.

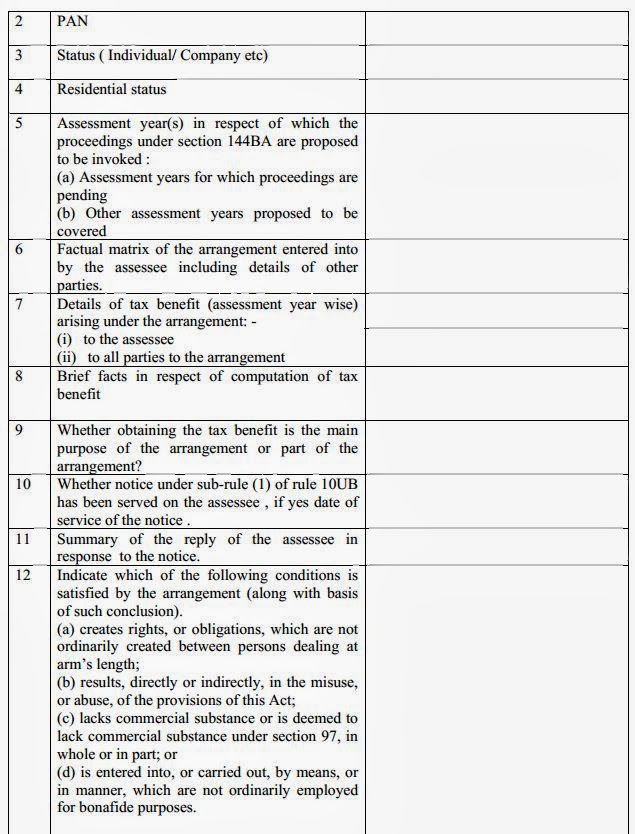

(2) The notice referred to in sub-rule (1) shall contain the following: -

(i) details of the arrangement to which the provisions of Chapter X-A are proposed to be applied;

(ii) the tax benefit arising under the arrangement;

(iii) the basis and reason for considering that the main purpose of the identified arrangement is to obtain tax benefit;

(iv) the basis and the reasons why the arrangement satisfies the condition provided in clause (a), (b),

(c) or (d) of sub-section (1) of section 96; and

(v) the list of documents and evidence relied upon in respect of (iii) and (iv) above.

(3) The reference by the Assessing Officer to the Commissioner under sub-section

(1) of section 144BA shall be in Form No.3CEG.

(4) Where the Commissioner is satisfied that the provisions of Chapter X-A are not

required to be invoked with reference to an arrangement after considering –

(i) the reference received from the Assessing Officer under sub-section (1) of

section 144BA; or

(ii) the reply of the assessee in response to the notice issued under sub-section (2) of section 144BA,

he shall issue directions to the Assessing Officer in Form No. 3CEH.

(5) Before a reference is made by the Commissioner to the Approving Panel under

sub-section (4) of section 144BA, he shall record his satisfaction regarding the

applicability of the provisions of Chapter X-A in Form No. 3CEI and enclose the same

with the reference.

Time limits.

10UC. (1)For the purposes of section 144BA,–

(i) no directions under sub-section (3) of section 144BA shall be issued

by the Commissioner after the expiry of one month from the end of

the month in which the date of compliance of the notice issued

under sub-section (2) of section 144BA falls;

(ii) no reference shall be made by the Commissioner to the Approving

Panel under sub-section (4) of section 144BA after the expiry of two

months from the end of the month in which the final submission of

the assessee in response to the notice issued under the subsection(2) of section 144BA is received;

(iii) the Commissioner shall issue directions to the assessing officer in

Form No.3CEH, -

(a) in the case referred to in clause (i) of sub-rule (4) of rule 10UB, within a period of one month from the end of month in which the reference is received by him; and

(b) in the case referred to in clause (ii) of sub-rule (4) of rule

10UB, within a period of two months from the end of month

in which the final submission of the assessee in response to

the notice issued under sub-section (2) of section 144BA is

received by him.”;

(b) in Appendix-II, after Form No. 3CEF, the following Forms shall be inserted, namely:-

SOURCE - CLICK HERE TO VIEW

[TO BE PUBLISHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II,

SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

[CENTRAL BOARD OF DIRECT TAXES]

Notification

New Delhi, the 23rd day of September, 2013

INCOME-TAX

S.O. 2887(E).- In exercise of the powers conferred by sections 101 and144BA read with

section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby

makes the following rules further to amend the Income-tax Rules, 1962, namely:-

1. (1) These rules may be called the Income-tax (17th Amendment) Rules, 2013.

(2) They shall come into force on the 1st day of April, 2016.

2. In the Income-tax Rules, 1962, –

(a) after rule 10T, the following rules shall be inserted, namely: -

“ DA. Application of General Anti Avoidance Rule

Chapter X-A not to apply in certain cases

10U. (1) The provisions of Chapter X-A shall not apply to -

(a) an arrangement where the tax benefit in the relevant assessment

year arising, in aggregate, to all the parties to the arrangement does

not exceed a sum of rupees three crore;

(b) a Foreign Institutional Investor, –

(i) who is an assessee under the Act;

(ii) who has not taken benefit of an agreement referred to in

section 90 or section 90A as the case may be; and

(iii) who has invested in listed securities, or unlisted securities,

with the prior permission of the competent authority, in

accordance with the Securities and Exchange Board of India

(Foreign Institutional Investor) Regulations, 1995 and such

other regulations as may be applicable, in relation to such

investments;

(c) a person, being a non-resident, in relation to investment made by

him by way of offshore derivative instruments or otherwise,

directly or indirectly , in a Foreign Institutional Investor;

(d) any income accruing or arising to, or deemed to accrue or arise to,

or received or deemed to be received by, any person from transfer

of investments made before the 30th day of August, 2010 by such

person.

(2) Without prejudice to the provisions of clause (d) of sub-rule (1), the provisions of

Chapter X-A shall apply to any arrangement, irrespective of the date on which it

has been entered into, in respect of the tax benefit obtained from the arrangement

on or after the 1st. day of April, 2015.

(3) For the purposes of this rule, -

(i) “Foreign Institutional Investor” shall have the same meaning as assigned to

it in the Explanation to section 115AD;

(ii) “off shore derivative instrument” shall have the same meaning as assigned to it in the Securities and Exchange Board of India ( Foreign Institutional Investor) Regulations, 1995 issued under Securities and Exchange Board of India Act, 1992 (15 of 1992) ;

(iii) “Securities and Exchange Board of India” shall have the same meaning as assigned to it in clause (a) of sub-section (1) of section 2 of the Securities and Exchange Board of India Act, 1992 (15 of 1992);

(iv) “tax benefit” as defined in clause (10) of section 102 and computed in

accordance with Chapter X-A shall be with reference to-

(a) sub-clauses (a) to (e) of the said clause , the amount of tax; and

(b) sub-clause (f) of the said clause, the tax that would have been

chargeable had the increase in loss referred to therein been the total

income.

Determination of consequences of impermissible avoidance arrangement.

10UA . For the purposes of sub-section (1) of section 98, where a part of an arrangement

is declared to be an impermissible avoidance arrangement, the consequences in relation

to tax shall be determined with reference to such part only.

Notice, Forms for reference under section 144BA

10UB. (1)For the purposes of sub-section (1) of section 144BA, the Assessing

Officer shall, before making a reference to the Commissioner, issue a notice in writing to

the assessee seeking objections, if any, to the applicability of provisions of Chapter X-A

in his case.

(2) The notice referred to in sub-rule (1) shall contain the following: -

(i) details of the arrangement to which the provisions of Chapter X-A are proposed to be applied;

(ii) the tax benefit arising under the arrangement;

(iii) the basis and reason for considering that the main purpose of the identified arrangement is to obtain tax benefit;

(iv) the basis and the reasons why the arrangement satisfies the condition provided in clause (a), (b),

(c) or (d) of sub-section (1) of section 96; and

(v) the list of documents and evidence relied upon in respect of (iii) and (iv) above.

(3) The reference by the Assessing Officer to the Commissioner under sub-section

(1) of section 144BA shall be in Form No.3CEG.

(4) Where the Commissioner is satisfied that the provisions of Chapter X-A are not

required to be invoked with reference to an arrangement after considering –

(i) the reference received from the Assessing Officer under sub-section (1) of

section 144BA; or

(ii) the reply of the assessee in response to the notice issued under sub-section (2) of section 144BA,

he shall issue directions to the Assessing Officer in Form No. 3CEH.

(5) Before a reference is made by the Commissioner to the Approving Panel under

sub-section (4) of section 144BA, he shall record his satisfaction regarding the

applicability of the provisions of Chapter X-A in Form No. 3CEI and enclose the same

with the reference.

Time limits.

10UC. (1)For the purposes of section 144BA,–

(i) no directions under sub-section (3) of section 144BA shall be issued

by the Commissioner after the expiry of one month from the end of

the month in which the date of compliance of the notice issued

under sub-section (2) of section 144BA falls;

(ii) no reference shall be made by the Commissioner to the Approving

Panel under sub-section (4) of section 144BA after the expiry of two

months from the end of the month in which the final submission of

the assessee in response to the notice issued under the subsection(2) of section 144BA is received;

(iii) the Commissioner shall issue directions to the assessing officer in

Form No.3CEH, -

(a) in the case referred to in clause (i) of sub-rule (4) of rule 10UB, within a period of one month from the end of month in which the reference is received by him; and

(b) in the case referred to in clause (ii) of sub-rule (4) of rule

10UB, within a period of two months from the end of month

in which the final submission of the assessee in response to

the notice issued under sub-section (2) of section 144BA is

received by him.”;

(b) in Appendix-II, after Form No. 3CEF, the following Forms shall be inserted, namely:-

{kind=link}

0 comments